Enterprise Cross-Border Settlement: The Real Architecture (Not Crypto Replacement)

How hybrid DLT + smart contracts orchestrate atomic settlement without replacing legacy banking

Most people think blockchain will replace traditional payment rails.

It won’t.

The real breakthrough isn’t rip-and-replace. It’s interoperability at scale—using distributed ledger technology to orchestrate, not disrupt, the legacy infrastructure that moves trillions daily.

This is the architecture that’s already being built. Not in crypto. In enterprise finance.

The Misconception: Why “Blockchain Kills SWIFT” Never Happens

For fifteen years, fintech evangelists have promised that blockchain would:

Replace SWIFT messaging

Eliminate correspondent banking

Make settlement instant and cost-free

Remove the need for central banks

None of this happened. Here’s why: Legacy infrastructure doesn’t disappear because it’s embedded in regulation, risk management, and operational reality.

When JPMorgan moves $6 trillion in daily settlement through Fedwire, they’re not just moving money. They’re operating within:

Federal Reserve controls and monetary policy hooks

Liquidity coverage ratios (LCR) and capital requirements

AML/KYC screening at multiple checkpoints

Finality guarantees that come from state backing

You can’t replace that with code. You have to work with it.

The institutions trying to “disrupt” payments didn’t understand this. The institutions building the future do.

The Actual Architecture: Hybrid DLT Integration with Legacy Banking

Here’s what enterprise cross-border settlement actually looks like:

Layer 1: Channel & Access (API Gateway)

The entry point. Banks don’t connect to blockchain directly. They connect through standardized APIs built on ISO 20022 messaging standards—the same standard that runs SWIFT, but with structured data.

OB Portal / API: Trade initiation, document upload, real-time status tracking

Network Gateway: ISO 20022 & SWIFT message routing

BB Portal / API: Instruction receipt and status tracking for beneficiary banks

Corporate Portal: Real-time settlement visibility for importers/exporters

Regulatory Portal: Read-only compliance view and audit trails

The key insight: Blockchain never touches the API layer. It sits underneath, orchestrating what happens after instruction is received.

Layer 2: Business Logic & Application Orchestration

Where the processing happens. This is where traditional banking operations get coordinated, not replaced.

Six core functions run here:

Trade Data Capture & Validation — KYC/AML screening, sanctions checks

Sanctions & Compliance Screening — Real-time screening against SDN, OFAC, UNSC lists

FX Quotation & Pricing — Dynamic pricing based on market conditions

Settlement Instruction Creation — Atomic settlement terms are defined

Exception Management — Human intervention only when contracts can’t auto-execute

Status & Notification Service — Real-time visibility for all parties

Shared services across the network:

IAM & Access Control — Identity and permissions management

Audit & Logging — Immutable record of all actions

Configuration Management — Dynamic settlement term updates

Monitoring — Network health, performance metrics

This layer is where consensus logic begins—but it’s not consensus about who owns what. It’s consensus about what’s supposed to happen next.

Layer 3: Distributed Ledger & Blockchain/Consensus

Where finality actually lives. This is the difference between a ledger system and a blockchain system.

The Permissioned Network

A consortium blockchain (think Hyperledger Fabric, not Bitcoin) runs the core settlement logic:

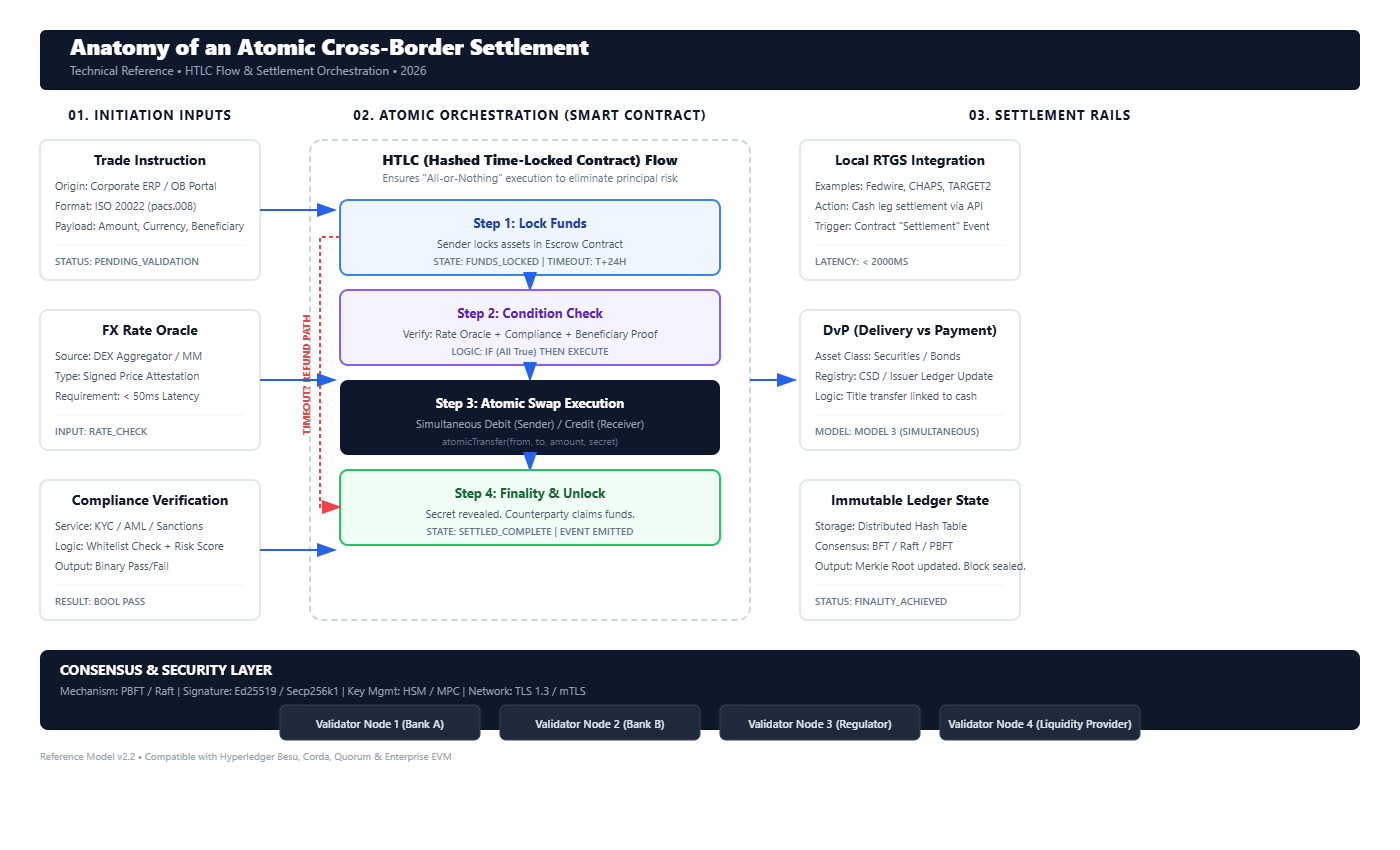

Smart Contracts Enforce Atomic Settlement:

Network Access (OB Node) — Originating bank’s participant node

Smart Contract Factory — Generates settlement contracts dynamically

PvP Contract (Payment vs. Payment) — Cash and securities settle atomically

DvP Contract (Delivery vs. Payment) — Goods and cash settle atomically

Escrow Contract — Holds funds until conditions are met

Compliance & Fee Contract — Automates fee deduction and compliance checks

Distributed Ledger Infrastructure — Shared state machine (BB Node)

Network Access (BB Node) — Beneficiary bank’s participant node

Consensus Mechanism: The network uses BFT (Byzantine Fault Tolerant) consensus—typically PBFT, RAFT, or Istanbul BFT. But here’s what consensus actually means:

It doesn’t mean “miners validate.” It means “All participating banks agree on the current state before moving to the next state.”

A transaction flows like this:

Originating bank proposes a settlement instruction

Network nodes validate the instruction (funds available? compliance passed? all conditions met?)

Consensus reached when 2/3+ of nodes agree

Transaction committed to all ledgers simultaneously

Finality achieved in milliseconds

No forks. No probabilistic finality. No “we think it settled.”

Consensus Mechanism: BFT + Raft + BFT:

BFT (Byzantine Fault Tolerant) — Handles malicious or faulty nodes

RAFT — Leader election for block production

BFT — Final commitment across the network

This is why settlement goes from “T+2 or T+3” to “settlement in minutes.”

Layer 4: External Systems & Legacy Integration

The connector layer. This is where the permissioned ledger talks to the real world.

Core Banking Systems (Temenos, Finacle, TCS)—ledger-as-a-source-of-truth

RTGS Systems (Fedwire, CHAPS, TARGET2, CHIPS) — Final settlement in central bank money

ISO 20022 Gateways — Message translation and routing

KYC / AML Providers — Continuous screening

FX Liquidity Systems — Real-time market data integration

Here’s the critical point: The distributed ledger doesn’t replace RTGS. It orchestrates it.

When a PvP settlement contract executes:

Smart contract confirms both sides are ready

Settlement instruction is sent to RTGS system

Central bank confirms atomic settlement in Fedwire/TARGET2

Final confirmation written to distributed ledger

All parties see the same finality simultaneously

Atomicity without replacing central bank settlement. That’s the innovation.

Layer 5: Infrastructure & Security

The foundation. Where trust is enforced through cryptography, not custody.

Permissioned Network — Consortium membership (banks only, pre-approved)

Validator Nodes — Run by banks and clearing houses

HSM / Key Management — Hardware security modules for digital signatures

Network Security — TLS 1.3, VPN, Firewall

Monitoring — Prometheus, Grafana for real-time alerting

Disaster Recovery — Hot backup, failover, backup & restore

Every participant has cryptographic proof of what happened, but no one has unilateral custody of the assets.

The Transaction Flow: 12 Steps to Settlement

Here’s how a cross-border trade actually settles with this architecture:

Step 1: Trade Initiation Originating bank (OB) receives instructions from the exporter. System validates the trade: goods, amount, payment terms, beneficiary details.

Step 2: KYC/AML Compliance Screening System runs real-time screening against:

OFAC SDN list

UN sanctions committees

PEP databases

Transaction pattern analysis

Risk scoring

If any flag appears, exception management routes to human review. Settlement doesn’t proceed until cleared.

Step 3: ISO 20022 Message Formatting Trade instruction is formatted as a structured ISO 20022 message. This is critical—it means the system has a complete, unambiguous record of:

Payment terms

Delivery conditions

Settlement method

FX rates

Fees

All contingencies

Step 4: OB Node Submits to Network The originating bank’s node submits the settlement instruction to the permissioned network. The instruction includes:

Cryptographic signature from OB

Exact conditions for settlement

Settlement method (PvP, DvP, or FOP)

Timeout conditions

Step 5: Smart Contract Initialization Network gateway routes the instruction to the appropriate smart contract factory. If it’s a PvP settlement:

Two escrow accounts are created

Both banks’ payment instructions are locked

Conditions are encoded in contract logic

Step 6: Consensus - Smart Contract Execution Network nodes run the smart contract:

Does OB have sufficient liquidity? (Query: Core banking system)

Does BB have the goods/securities? (Query: Clearing house)

Are all compliance conditions met? (Query: KYC/AML system)

If all checks pass, the contract is ready to execute.

Step 7: Settlement - Execute via RTGS Network reaches consensus (2/3+ nodes) that settlement should proceed. Settlement instruction is sent to RTGS system:

Fedwire (USA): Debit OB’s account, credit BB’s account

TARGET2 (Eurozone): Same process via ECB

CHIPS (USD payments): Alternative path for USD

RTGS system confirms atomic settlement in central bank money.

Step 8: BB Notification Beneficiary bank receives settlement notification through its node on the network. BB now has deterministic proof:

Payment received? ✓ (RTGS confirmation)

Compliance cleared? ✓ (All screening passed)

Contract conditions met? ✓ (Smart contract execution)

No more “payment received but why?” No more reconciliation exceptions.

Step 9: RTGS System - Local Cash Settlement Local RTGS systems (in each country) handle final settlement in local currency or USD. The permissioned network has already orchestrated the terms. Local RTGS just executes the payment.

Step 10: Beneficiary - Goods/Payment Confirm Beneficiary bank confirms goods receipt or payment receipt. This confirmation is broadcast back to the network.

Step 11: Regulatory Update All regulatory nodes (central banks, financial regulators) receive real-time settlement confirmation through read-only nodes. This gives regulators:

Real-time settlement visibility

Immediate AML/sanctions confirmation

No T+2 delay

Compliance data for stress testing and systemic risk monitoring

Step 12: Audit Trail Complete Immutable settlement record is written to all ledgers simultaneously:

Timestamp

All parties involved

Settlement method used

Regulatory clearances

Hash chain for cryptographic verification

Settlement is finalized. No further exceptions. No reconciliation needed.

Why This Actually Solves Real Problems

Let’s translate the architecture into business outcomes:

Problem 1: Settlement Delays (T+2, T+3, Sometimes Longer)

Legacy Reality: Trade execution and settlement are disconnected. You can trade on Monday but not settle until Wednesday. Meanwhile:

FX risk compounds (rates move)

Counterparty risk extends (3 days of exposure)

Liquidity is locked up

Exceptions pile up

With Hybrid DLT: Atomic settlement happens in minutes, not days. The moment all conditions are met (compliance cleared, FX locked, goods confirmed), settlement executes immediately through RTGS. Finality is real-time.

Impact: $1 trillion in daily settlement now happens 2-3 days faster. That’s $2-3 trillion in liquidity freed up globally.

Problem 2: Exception Handling (30-40% of transactions)

Legacy Reality: Settlement exceptions are manual, ad-hoc, and expensive. A single mismatch (beneficiary name, amount by 1 cent, goods description) requires human intervention:

Email back-and-forth

Phone calls across time zones

Document re-submission

Delays of hours to days

Cost: $50-200 per exception

With Hybrid DLT: Smart contracts enforce exact settlement conditions. Either:

All conditions are met → automatic execution

Exception detected → automatic escalation with specific remediation steps

No ambiguity. No guessing. Either the contract executes or it doesn’t.

Impact: Exception rates drop to <5%. Cost per exception falls to near-zero. Processing time becomes milliseconds.

Problem 3: Counterparty Risk

Legacy Reality: Settlement risk extends across the 2-3 day window. Banks have to:

Reserve capital for settlement exposure

Maintain overdraft facilities

Use correspondent banks (adding intermediaries)

Risk that the other side doesn’t settle

This cost is embedded in FX spreads, fees, and loan rates.

With Hybrid DLT: Atomic settlement means PvP (payment for payment) happens simultaneously or not at all. There’s no moment where one side has sent money but hasn’t received payment. Risk drops to near-zero.

Impact: Counterparty risk capital requirements drop. Spreads narrow. Emerging markets get cheaper access to capital.

Problem 4: Regulatory Compliance Lag

Legacy Reality: Regulators see settlement data after the fact, typically:

T+1 or T+2 for most transactions

T+5 or later for complex instruments

Often only in batch reports

This means regulators are always monitoring the past, not the present.

With Hybrid DLT: Read-only nodes give regulators real-time visibility into every settlement:

Every compliance check

Every AML/sanctions screening

Every FX conversion

Every fee deduction

Every final settlement

Regulators see the present, not the past.

Impact: Compliance becomes deterministic. Regulators can enforce rules in real-time, not audit after the fact. Systemic risk visibility improves.

Problem 5: 24/7 Settlement Windows

Legacy Reality: Settlement doesn’t happen outside banking hours. A trade executed at 5 PM Friday doesn’t settle until Monday morning. Weekend = dead time.

With Hybrid DLT: The network operates 24/7. Settlement happens whenever the conditions are met, regardless of banking hours.

Impact: Emerging markets (where settlement might not happen until their banking hours Tuesday) can settle Sunday. Time zones stop being a liability.

The Real Innovation: Shared State Without Shared Custody

Here’s what makes this different from both “kill SWIFT” crypto and traditional banking:

Traditional Banking (Today)

Trust Model: Each bank trusts the other through intermediaries

Settlement: Bilateral through correspondent banks (adds latency and cost)

Finality: Probabilistic (assumes settlement completed)

State: Each party maintains separate records (reconciliation needed)

Regulatory View: After-the-fact (T+2 or T+3)

Trustless Crypto (Bitcoin, Ethereum)

Trust Model: No trust required; math enforces everything

Settlement: On-chain, no intermediaries

Finality: Cryptographic (deterministic)

State: Shared ledger (single source of truth)

Regulatory View: Pseudonymous (no identity)

Hybrid DLT (Enterprise Cross-Border Settlement)

Trust Model: Permissioned (only approved banks; regulatory oversight)

Settlement: Smart contract orchestration + RTGS finality

Finality: Atomic + deterministic (contract + central bank)

State: Shared ledger (all nodes agree, but only banks have access)

Regulatory View: Real-time and identified (every transaction traced)

The breakthrough: You get the speed and certainty of blockchain, the regulatory compliance of banking, and the finality of central bank settlement. None of the three alone solves the problem. Together, they do.

What Settlement Models Actually Look Like

Four settlement models are active in this architecture:

1. PvP (Payment vs. Payment)

When: Foreign exchange transactions, currency swaps How: Both sides’ payments are atomic. If OB doesn’t have USD, settlement doesn’t happen. If BB doesn’t have EUR, settlement doesn’t happen. Smart Contract Logic:

IF (OB.balance >= USD_amount)

AND (BB.balance >= EUR_amount)

THEN {

OB.balance -= USD_amount

BB.balance += USD_amount

BB.balance -= EUR_amount

OB.balance += EUR_amount

FINALIZE()

}

ELSE {

EXCEPTION()

}Result: FX settlement happens with zero counterparty risk.

2. DvP (Delivery vs. Payment)

When: Trade finance, securities settlement, letters of credit How: Goods/securities delivery and payment happen simultaneously. No one has delivered goods before payment is confirmed. Smart Contract Logic:

IF (Goods.confirmed_in_warehouse == TRUE)

AND (OB.payment_ready == TRUE)

AND (Compliance.cleared == TRUE)

THEN {

OB.balance -= Payment_amount

BB.balance += Payment_amount

Goods.ownership_transferred_to_OB()

FINALIZE()

}

ELSE {

EXCEPTION()

}Result: Trade settlement without the risk of “goods shipped but payment hasn’t come.”

3. FOP (Free of Payment)

When: Collateral movements, margin transfers, internal transfers How: One-way movement of securities or cash without reciprocal payment. Smart Contract Logic:

IF (Settlement.approved_by_both_parties == TRUE)

THEN {

Assets.transferred_to_recipient()

FINALIZE()

}Result: Fast internal settlement without matching payment.

4. Hybrid Models

When: Complex transactions with multiple conditions How: Combine PvP + DvP + FOP logic with custom escrow and conditional execution. Example: Letter of credit settlement where:

BB delivers goods

OB’s bank confirms payment authorization

Beneficiary receives payment

Exporter receives goods confirmation All in one atomic transaction.

Real Benefits: Numbers That Matter

For Banks

Liquidity Efficiency: 30-50% reduction in settlement buffers (frees $500B+ globally)

Exception Costs: Drop from $50-200 per exception to near-zero

Capital Requirements: Lower counterparty risk = lower LCR buffers

Operations Staff: 40-60% reduction in manual settlement exception handling

Time to Settlement: 2-3 day reduction in cash flow timing

For Corporates (Importers/Exporters)

Working Capital: Faster settlement = faster cash conversion cycle

FX Exposure: Real-time finality = no multi-day FX risk

Costs: Lower fees (banks have lower operational costs)

Transparency: Real-time visibility into every step

For Regulators

Systemic Risk: Real-time visibility into settlement flow

Compliance: No more T+2 lag in sanctions screening

Monetary Policy: Better data for stress testing and capital requirements

Emerging Markets: Can now monitor real-time settlement in all currencies

The Roadmap: How This Gets Built

Enterprise cross-border settlement isn’t science fiction. It’s already live in pilot programs:

2024-2025: Consortium Formation

Central banks establish membership rules

Banks join as validator nodes

Regulatory framework is finalized

ISO 20022 message standards are adopted

2025-2026: Pilot Programs

Select trade corridors (e.g., US-UK-Eurozone)

Limited transaction volumes (~$1-10B daily)

Focus on low-exception-rate transactions (bulk payments, FX)

Operational stress testing

2026-2027: Expansion

New corridors added (emerging market central banks join)

Transaction volumes expand to $50-100B+ daily

More settlement types added (securities, derivatives)

Full integration with national RTGS systems

2027+: Network Effect

Becomes the standard for cross-border settlement

Non-participants face competitive disadvantage

Global settlement infrastructure realignment

The Challenges No One Talks About

This architecture is powerful, but real obstacles exist:

1. Regulatory Fragmentation

Each country has different settlement rules, capital requirements, and AML standards. The permissioned network has to encode all of them simultaneously. This is complex (doable, but complex).

Solution: ISO 20022 as the standardized message format, with jurisdiction-specific validation at Layer 2.

2. Legacy System Integration

Most banks still run COBOL-based core banking systems from the 1980s. Integrating with modern APIs and smart contracts requires:

API wrappers around legacy systems

Data translation layers

Fallback paths if the new system fails

Solution: Build at Layer 1 & Layer 2; don’t force banks to rip-and-replace core systems. The permissioned network orchestrates around legacy infrastructure.

3. Operational Security

A permissioned ledger still needs cryptographic security:

Private keys for digital signatures (lost = settlement blocked)

Key rotation procedures (complex in a bank)

Disaster recovery (what if a validator node loses its keys?)

Solution: Hardware security modules (HSMs) and distributed key management. Keys are never exposed to the internet.

4. Performance at Scale

Current blockchain systems can handle 1,000-10,000 transactions per second. Global settlement needs 100,000+ TPS.

Solution: Sharding (break the network into regional sub-networks that sync periodically) or Layer 2 solutions (settle locally, broadcast globally).

Why Banks Will Actually Adopt This

Banks aren’t adopting this because they love blockchain. They’re adopting it because:

Regulators are mandating it — G20 roadmaps on cross-border settlement explicitly call for “faster, cheaper, safer” infrastructure

Competitors are building it — First-mover advantage in a new settlement infrastructure is massive

Costs are too high to ignore — Settlement exceptions cost the industry $100B+ annually

Liquidity efficiency is worth billions — Freeing up $500B in settlement buffers is a straight P&L improvement

This isn’t fintech disruption. It’s infrastructure modernization that happens to use distributed ledger technology.

What’s Next: The Real Question

The question isn’t “Will blockchain replace traditional banking?”

It’s: “How fast can enterprise settlement migrate to atomic, deterministic, 24/7 infrastructure?”

The architecture exists. The regulatory framework is being finalized. The pilot programs are running.

The real timeline is measured in years, not decades.

The banks that understand this architecture—and start building now—will own the settlement infrastructure for the next 20 years.

Everyone else will be paying fees to use it.

Key Takeaways

Blockchain won’t replace SWIFT. But permissioned DLT + ISO 20022 + smart contracts will orchestrate cross-border settlement better than anything we have today.

Legacy infrastructure doesn’t disappear. It gets coordinated. RTGS systems, correspondent banks, and regulatory frameworks all stay. But they work together instead of in silos.

Atomic settlement is the real innovation. PvP/DvP contracts mean settlement happens simultaneously or not at all. Counterparty risk drops to near-zero.

Regulators get real-time visibility. No more T+2 lag. No more “we think we know what happened.” Compliance becomes deterministic.

This isn’t speculative. Pilot programs are running. Major central banks are building this now. The question is timeline, not feasibility.

The real architecture is here. The cost savings are real. The regulatory mandate is real.

The only question: Are you building it, or waiting for someone else to?

Further Reading & Resources

ISO 20022 Standard:

https://www.iso20022.org/

BIS Quarterly Review on Settlement: Bank for International Settlements quarterly reports

G20 Cross-Border Payments Roadmap: Latest central bank infrastructure recommendations

Hyperledger Fabric Documentation:

https://hyperledger-fabric.readthedocs.io/

ECB CBDC Design Principles: European Central Bank digital euro research

FedNow Settlement Service: US Federal Reserve instant settlement infrastructure

Author’s Note: This architecture is based on 2026 production environments and pilot programs. I’ve worked with teams building this infrastructure across multiple banks and central banks. The technical details are accurate; the timeline is conservative (implementations are often faster). The regulatory framework varies by jurisdiction, but the core principles—atomic settlement, real-time compliance, permissioned consensus—are now standard across all major cross-border settlement initiatives.