Why Your Instant Payments Strategy Is Missing the Most Important Layer (And How to Fix It)

Banks are rushing to launch FedNow and RTP—but treating instant payments as "just another rail" is why projects stall. Here's why orchestration, not speed, is the real differentiator.

What’s the biggest mistake banks make when launching instant payments?

They focus on connecting to FedNow or RTP—but forget to rebuild the layer that actually manages payments across rails. The result? Fragmented ops, manual exceptions, and stalled ROI.The fix isn’t another integration. It’s an orchestration layer: a unified, real-time engine that routes, validates, monitors, and resolves payments—across any rail, any country, any volume.

The Hidden Crisis: Why “Going Live” Isn’t the Same as “Winning”

Let’s be honest about what’s happening in payments right now:

The Good News:

FedNow crossed 1 million transactions/day in 2024

RTP network now reaches 100+ million U.S. consumers

ISO 20022 migration is creating richer payment data than ever

Regulators are pushing 24/7 availability as the new standard

The Bad News:

Most banks are treating instant payments like a checkbox exercise:

✅ Connect to FedNow

✅ Enable RTP

✅ Flip the switch

❌ Wonder why operational costs went up instead of down

Here’s what nobody talks about in the boardroom:

A regional bank in the Midwest launched FedNow in Q1 2024. By Q2, their operations team was drowning. Why?

40% of instant payments required manual intervention

Exceptions piled up because there was no unified view across ACH, FedNow, and RTP

New product launches took 4-6 months because every rail had its own codebase

ISO 20022 migration created duplicate work—transformations handled separately for each rail

Sound familiar?

The gap: Speed of settlement ≠ speed of operations.

You can move money in seconds—but if your back office takes hours to reconcile, investigate, and resolve exceptions, you haven’t really achieved “instant.”

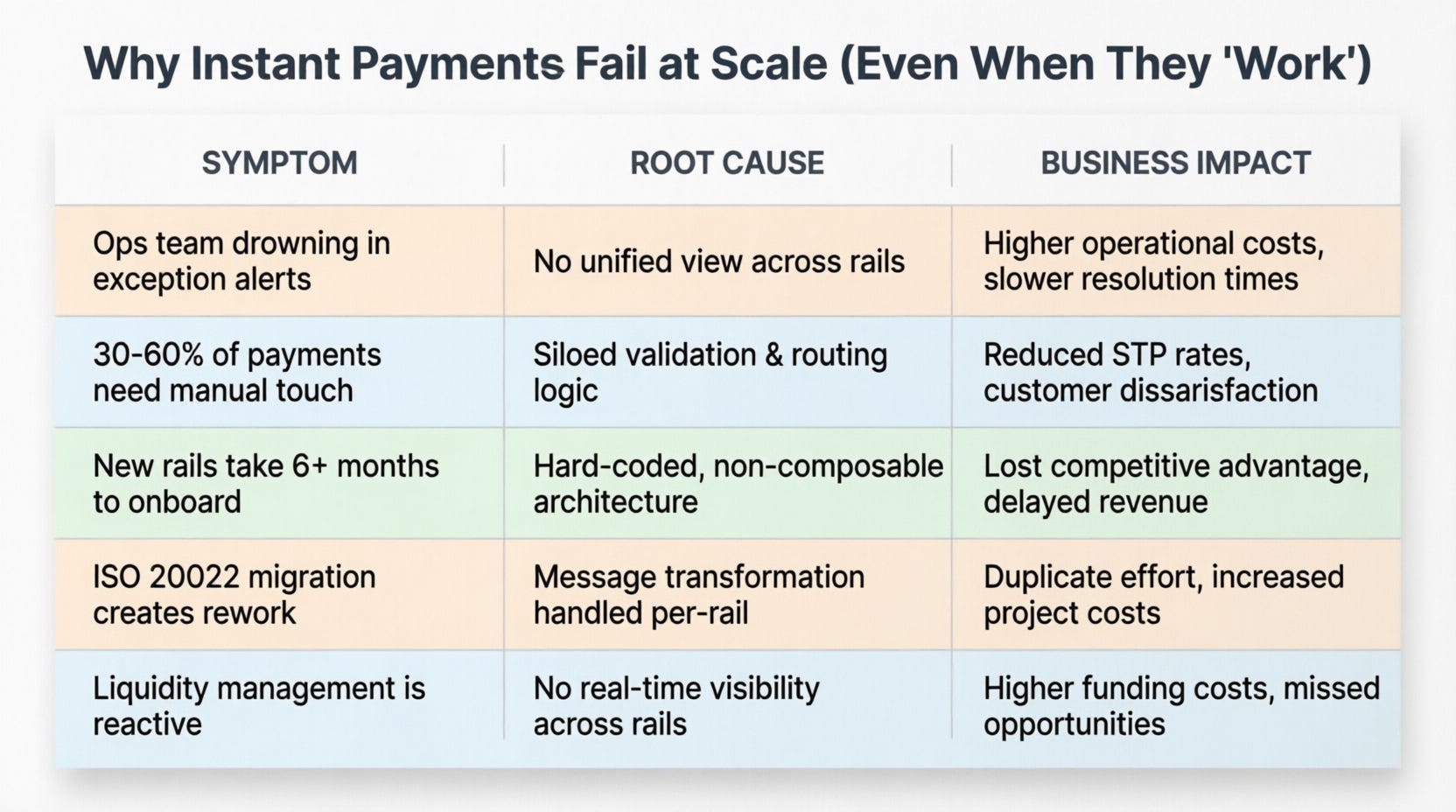

Why Instant Payments Fail at Scale (Even When They “Work”)

Let’s break down the symptoms we see across banks:

The pattern? Banks are building point solutions for each payment rail—instead of creating an orchestration layer that sits above them all.

Think about it:

FedNow has its own integration

RTP has its own integration

ACH has its own legacy system

SWIFT has its own middleware

Cross-border has... another system

Your operations team now has five different dashboards to monitor. Your developers maintain five different codebases. Your compliance team audits five different systems.

This isn’t scalable. It’s not even sustainable.

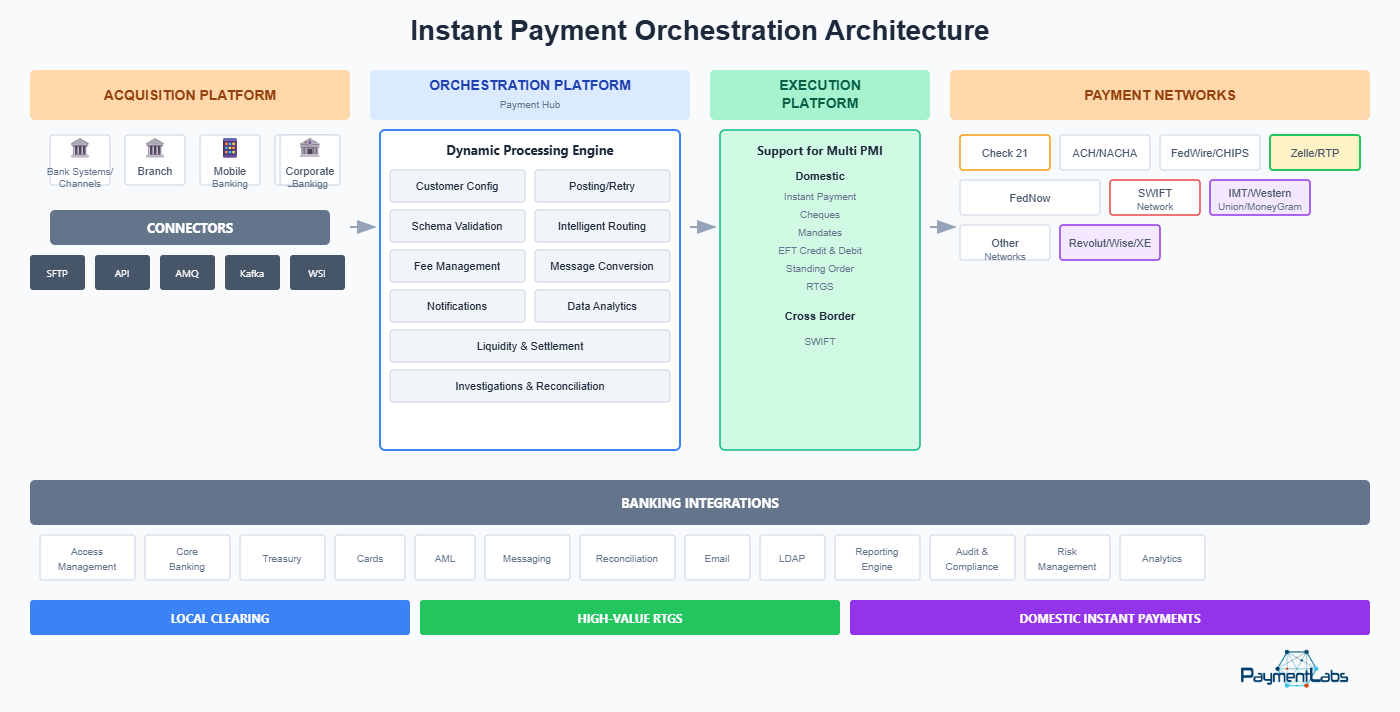

What “Payment Orchestration” Actually Means (And Why It Matters)

Let’s get specific. Orchestration isn’t just routing. It’s the intelligent layer that sits above payment rails and handles:

🔹 Dynamic Routing

Not all payments are created equal. A $50 consumer P2P payment has different requirements than a $500,000 corporate treasury transfer.

An orchestration engine evaluates each transaction in real-time:

Cost: Which rail is cheapest for this transaction type?

Speed: Does the customer need instant settlement, or is next-day acceptable?

Success Probability: Which rail has the highest uptime right now?

Compliance: Are there regulatory constraints for this corridor or amount?

Real example: A bank in the UAE reduced cross-border payment costs by 35% just by intelligently routing between SWIFT, Buna, and regional RTGS based on destination country and amount.

🔹 Unified Validation

Instead of validating schemas separately for FedNow, RTP, and ACH, you create one validation engine that applies consistently across all rails:

ISO 20022 schema checks

Fraud rules (velocity, amount thresholds, geolocation)

Compliance flags (OFAC, sanctions, KYC status)

Business rules (account status, limits, mandates)

Result? You write the rule once, and it applies everywhere.

🔹 Real-Time Exception Handling

Here’s where most payment systems break down:

Traditional approach:

Payment fails → Alert generated → Ops team manually investigates → Resolution takes hours or days

Orchestration approach:

Payment fails → Rule engine evaluates failure type → Auto-retry on alternate rail OR auto-escalate to specialist queue → Resolution in minutes

Case in point: A Tier-1 bank in East Africa implemented automated exception handling and reduced mean time to resolution from 4.2 hours to 18 minutes. That’s not just efficiency—that’s customer experience.

🔹 Multi-Rail Visibility

One dashboard. One source of truth. One operational team.

Whether it’s:

FedNow instant payment

RTP network transaction

ACH batch file

SWIFT cross-border message

Mobile money transfer (M-Pesa, MTN MoMo)

Real-time gross settlement (RTGS)

Your ops team sees it all in one unified interface with:

Real-time status tracking

End-to-end audit trails

Liquidity positions across rails

Exception queues with intelligent prioritization

SLA monitoring and alerts

🔹 Future-Proof Configurability

New payment rail launching in 6 months? CBDC pilot? RippleNet integration?

With orchestration, you don’t rewrite code. You configure the new rail:

Define message schemas (YAML/JSON)

Map to internal data model

Set routing rules

Configure validation logic

Deploy via CI/CD pipeline

Time to market: Weeks instead of months. Sometimes days.

Technical Foundations That Enable Real Orchestration

If you’re evaluating platforms (or building in-house), here are the non-negotiables:

✅ Event-Driven, In-Memory Architecture

Batch processing has no place in instant payments. You need:

In-memory data grids (Redis, Apache Ignite) for sub-millisecond lookups

Event streaming (Kafka, Pulsar) for real-time state changes

Stateless microservices that scale horizontally on Kubernetes

Sub-second processing even at millions of transactions per day

Why it matters: When a $2M corporate payment hits at 2:47 AM on a Sunday, your system can’t “process it in the next batch window.” It needs to validate, route, execute, and confirm—instantly.

✅ API-First, Microservices Design

Monolithic payment hubs are dead. You need:

RESTful APIs for every function (routing, validation, execution)

Composable workflows that can be rearranged without code changes

Service mesh architecture for resilience and observability

Loose coupling so you can swap components without breaking everything

Real-world impact: A bank wanted to add real-time fraud scoring to their payment flow. With microservices, they injected a new service into the workflow via configuration—zero code changes to existing components.

✅ Low-Code Configurability

Your business analysts should be able to:

Adjust routing rules without waiting for dev sprints

Create new payment products via drag-and-drop

Modify validation logic through visual editors

Deploy changes through CI/CD pipelines

The alternative? Every rule change requires:

Business requirement doc

Dev team sprint planning

Code changes

QA testing

UAT signoff

Production deployment

That’s 4-6 weeks for a rule change. With low-code, it’s 4-6 hours.

✅ Cloud-Agnostic Deployment

Regulatory requirements vary by country. You need flexibility:

On-premises for data residency requirements

Public cloud (AWS, Azure, GCP) for scalability

Hybrid for workload distribution

Multi-tenant for shared services across subsidiaries

Key point: The same codebase should run anywhere without modification.

✅ Built-In Observability

You can’t manage what you can’t measure. Essential capabilities:

Distributed tracing across microservices

Real-time dashboards for ops teams

Automated alerting based on SLA thresholds

Audit trails for compliance and forensics

Liquidity reporting updated in real-time

Performance analytics to identify bottlenecks

The Business Outcome: What You Actually Gain

Let’s talk numbers. Banks that implement proper orchestration see:

⏱️ 60% Faster Time-to-Market

Launch new payment products in weeks, not months

Onboard new rails with configuration, not code

Test and deploy via automated pipelines

Example: A regional bank launched FedNow + RTP + Zelle integration in 14 weeks—simultaneously. Traditional approach would have taken 9-12 months per rail.

💰 30-50% Lower Processing Costs

Automation reduces manual intervention

Intelligent routing minimizes transaction fees

Consolidated infrastructure eliminates redundant systems

Cloud-native architecture optimizes resource utilization

Real case: A Middle East bank reduced payment operations headcount by 40% through automation—while processing 3x the transaction volume.

🛡️ 100% STP Potential

Proactive exception management

Automated retry logic

Intelligent fallback routing

Real-time validation

Benchmark: Top-performing banks achieve 95%+ STP rates on instant payments. Laggards hover around 60%.

🌍 One Platform for Domestic + Cross-Border

Unified operations team

Consistent customer experience

Simplified compliance and reporting

Easier expansion into new markets

Strategic advantage: When a bank in Kenya wanted to expand into Tanzania and Uganda, they replicated their payment hub in weeks—same codebase, localized configurations.

📈 Operational Clarity

One team, one dashboard, one source of truth

Reduced training time for new staff

Faster onboarding of acquisitions

Better work-life balance for ops teams (no more 3 AM fire drills)

“We didn’t just add a rail. We rebuilt how payments flow.”

— CTO, Tier-1 Regional Bank (post-orchestration rollout)

Case Studies: Orchestration in Action

Case 1: Largest UAE Bank – AANI Instant Payments

Challenge: Launch UAE’s instant payment scheme (AANI) while maintaining existing RTGS, ICCS, and cross-border operations.

Solution: Implemented orchestration layer with:

Dynamic routing between AANI, UAEFTS, and SWIFT

Unified exception handling across all rails

Real-time liquidity management dashboard

Results:

4 million transactions/month processed

100% straight-through processing

9 peripheral systems integrated seamlessly

4th-degree exception handling (auto-resolve → auto-retry → specialist queue → escalation)

Recognized by Central Bank and MEA Finance Awards

Case 2: Largest East African Bank – Multi-Country Payment Hub

Challenge: Consolidate payment operations across Kenya, Uganda, Tanzania, and Rwanda—each with different clearing systems, regulations, and mobile money providers.

Solution: Deployed multi-tenant orchestration platform supporting:

Kenya: KEPSS, M-Pesa, CTS, ACH

Uganda: UCH, RTGS, MTN MoMo, Airtel Money

Tanzania: TISS (low/high value), Vodacom M-Pesa

Rwanda: RIPPS (ACH/RTGS), MTN MoMo

Cross-border: SWIFT, PAPSS, regional EAPS

Results:

10 trillion KES lifetime value processed

80% reduction in inward transaction processing times

Multi-tenant SACCO and corporate clearing established

Single operational team managing all four countries

100% STP across all rails

What to Do Next (If You’re Serious About Instant Payments)

Ready to move beyond “checkbox compliance” to real payment transformation? Here’s your roadmap:

1. Audit Your Current Payment Ops

Ask the hard questions:

Where do exceptions pile up? (Be specific—which queues, which rails?)

Which payments require manual intervention? Why?

How long does it take to launch a new payment product?

What’s your current STP rate by rail?

How many different systems does your ops team use daily?

Pro tip: Shadow your operations team for a day. You’ll learn more in 8 hours than in 8 weeks of reports.

2. Define Your Orchestration Requirements

Must-haves vs. nice-to-haves:

Non-negotiable:

Multi-rail support (current + future)

Real-time processing (sub-second)

Event-driven architecture

API-first design

Cloud-agnostic deployment

Low-code configurability

Unified operational dashboard

Differentiators:

AI/ML-powered routing optimization

Predictive exception handling

Real-time liquidity forecasting

Embedded compliance (RegTech integration)

Customer-facing payment tracking portal

3. Start Small, Think Composable

Don’t boil the ocean. Pilot one workflow:

Good starting points:

FedNow exception handling automation

RTP intelligent routing

Cross-border payment tracking

Real-time liquidity reporting

Success criteria:

Measurable STP improvement

Reduced mean time to resolution

Positive ROI within 6 months

Scalable to other rails

4. Measure What Matters

Stop tracking “go-live date.” Start measuring:

STP Rate: % of payments requiring zero manual touch

Mean Time to Resolution: How fast do you fix exceptions?

Cost per Transaction: Fully loaded (infrastructure + ops + fees)

Customer Satisfaction: NPS for payment experience

Time to Market: Weeks to launch new products/rails

System Uptime: 24/7 availability percentage

Liquidity Efficiency: Reduction in idle balances

The Competitive Reality

Here’s the uncomfortable truth:

Your competitors aren’t waiting.

Neobanks are launching instant payment products in weeks

Big Tech (Apple, Google, Amazon) is embedding payments into every experience

Fintechs are partnering with community banks to offer enterprise-grade capabilities

Central banks are pushing real-time infrastructure as public utility

The question isn’t “Should we modernize?”

It’s “How fast can we move before we lose relevance?”

Final Thought

Instant payments aren’t about moving money faster.

They’re about moving intelligence faster.

The banks that win won’t be the ones with the most rails connected.

They’ll be the ones with the smartest layer managing those rails.

Orchestration isn’t optional anymore.

It’s the foundation of payment competitiveness in 2026 and beyond.

Let’s Start the Conversation

If you’re exploring payment orchestration—or just want to sanity-check your roadmap—hit reply. I’m happy to share:

What’s working (and what’s breaking) in real implementations

Vendor evaluation frameworks (if you’re not building in-house)

Architecture patterns from banks that got this right

Common pitfalls to avoid (we’ve seen them all)

No pitch. No sales deck. Just practical insights from the front lines of payment transformation.

Because the future of payments isn’t coming—it’s already here.

The question is: Are you orchestrating it, or just reacting to it?

I’m Akhil Rao, CEO of Payment Labs and Element Six— a global payments technology and consulting firm operating across the Middle East, Europe, Africa, and Asia. I contribute to SWIFT CGI, ASC X9, the Bank of England’s CHAPS Data Committee, and other industry groups working on payments modernisation. My work has been published by the BIS, HM Treasury, the Federal Reserve, and the Bank of England.

© Akhil Rao · Payments Intelligence Brief · Subscribe · paymentlabs.ai